The first morning after arriving in China last week was the hardest. As I sipped an unusually strong blend of Chinese tea, reading the China Daily, I was pleased to see one of the lead articles describing in glorious detail the health benefits of tea, which evidently was first consumed in 2737 BC in China. Apparently, it has now been shown in a 25-year longitudinal study that tea drinkers had “better organized brain regions” which certainly sounded useful.

Obviously, it is a complicated time for an American to be in China, and absent one of my taxi drivers proclaiming deep affection for the President of the United States, most conversations steered quite clear of the geopolitical tensions. Frankly, it largely appeared to be business as usual, with a slight undercurrent of concern around general economic conditions. The 3Q19 economic growth rate of 6.0% was announced last week, a marked deceleration from prior quarters (although anecdotal evidence suggests actual growth rates may well be quite a bit lower). The state planning agency called the National Development and Reform Commission declared that this was due to an economy shifting from “rapid growth” to “high quality development.” Clearly, though, trade tensions are directly affecting cross-border transaction volumes.

Notwithstanding that the GDP growth rate over the last five years in China was 3x what was experienced in the United States, the MSCI China Index has increased only 18% versus the 50% increase of the S&P 500 Index over that same period. The International Monetary Fund is now forecasting 2019 global GDP growth to be 3.0% and China economic growth in 2024 to be 5.5%. Notably, the revenues of Chinese operations of U.S.-based companies will be $544 billion this year, underscoring the inter-dependencies of the two economies.

Analysts point to a number of factors for this deceleration including the financial drag caused by the central bank’s dominance of the financial system which tends to crowd out private companies in favor of state-owned enterprises. Clearly, the trade dispute looms ominously given the inconsistent progress after 13 rounds of bilateral talks. Issues including protection of intellectual property, cyber theft, government subsidies, and technology licensing (putting aside NBA tweets, turmoil in Hong Kong, the blacklisting of Chinese technology companies) ensure that the ultimate resolution is not even on the horizon. Barron’s estimates that the trade dispute will cost the global economy $770 billion in 2020, equivalent to the economy of Switzerland.

This week marks the start of the Communist Party’s Fourth Plenary Session of the 19th Central Committee, which is fraught with political intrigue. From such gatherings tend to come broad policy directives which analysts parse very carefully. Out of a similar session ten years ago it was decided with great fanfare that the Chinese renminbi (~7 RMB : $1 US) would play a greater (near equivalent) role in international trade as the U.S. dollar does to reduce China’s exposure to foreign exchange rate risk. Today, according to the Bank for International Settlements, 88% of all transactions involve the dollar while the RMB only accounts for 4%. Only 2% of total foreign exchange reserves are in RMB.

I was also interested in another article in the China Daily that provided progress on the 12th Five-Year Plan of the Healthcare Industry (2016-2020), which has three core tenets: increase the advancement of healthcare technologies, increase the capabilities of the domestic pharmaceutical industry, and drive increased consolidation. While the healthcare industrial complex in China is undergoing extraordinary reinvention to serve the needs of its 1.4 billion residents, centrally managing such a complicated system may at times appear ambitious, if not aspirational. Today, it is estimated that there are 300 million people who have chronic diseases and that by 2030 there will 360 million people over 60 years of age.

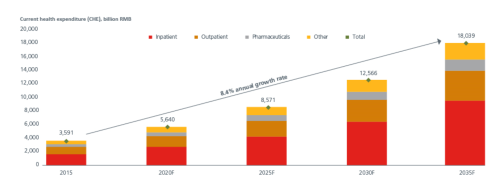

Even estimating the size of the Chinese healthcare market is complicated with at times quite divergent assessments. The research firm Eastspring China pegs the market in 2020 to be approximately $800 billion. Notwithstanding that, it is readily apparent that the opportunity is enormous given the stated priority of various central government directives and that it should naturally be on parity with other developing economies. China accounts for only 3% of global healthcare spend yet has 20% of the world’s population.

Per: Eastspring China (July 2019)

The 19th Central Committee has put forth its national healthcare strategy called “Healthy China 2030” which has set forth private commercial insurance as an essental component of a multi-level health security system. EY estimates that China spends slightly more than 6% of GDP on healthcare and that out-of-pocket is approximately 30% of that spend. There are 149 health insurance carriers operating in China that generated total health insurance premium revenue in 2017 was $62.7 billion. Between 2012 – 2017, the health insurance market grew at over 20% per annum.

The current single payor model with a high degree of government involvement has shown recently a willingness to experiment with novel payment and care models, even involving on a limited basis the private sector to participate. Some of the large successful internet companies (Alibaba, TenCent, etc.) are launching forays into healthcare, not unlike what is unfolding in the United States. According to Dezan Shira & Associates, a leading Asian business intelligence firm, the healthcare technology sector in China should reach $28.6 billion by 2026, which represents a 10-fold increase from 2016.

Given over 700 million Chinese now have smart phones and/or reliable access to the internet, critical early healthcare technology applications include delivery of online medical content, booking patient appointments, online payments, and accessing test results. Notably, the Organization of Economic Development estimates that there are only 1.8 doctors for every 1,000 people in China. There are 2,300 “top-tier” public hospitals and another 950,000 “low-tier” community health centers and clinics. The provider infrastructure is inadequate and must be augmented by innovative technology solutions.

Another article from the China Daily last week heralded the roll out of a centralized platform that inventoried all of the pharmaceutical industry assets in-country. Evidently there are 1,500 CROs, 3,500 pharma companies (although the China Chamber of Commerce estimates that there are 8,500 pharma companies and 16,000 medtech companies!), 2.37 million distinct healthcare products sold in China, and 50,000 healthcare investors.

A consistent theme echoed by healthcare industry leaders was the urgency to migrate from being principally a generics industry to a global leader in “first-in-class” novel therapeutics (95% of existing capacity is generics). According to the Chinese Academy of Sciences, between 2010 – 2018 more than 72% of novel therapeutic development was in the United States, while only 3% was in China. As part of this transition, there is a stated objective to shift to products and services that provide premium clinical benefits, a greater focus on ensuring equitable patient access, and to increase pharmacoeconomic value and affordability – not unlike much of the regulatory debate in the United States today.

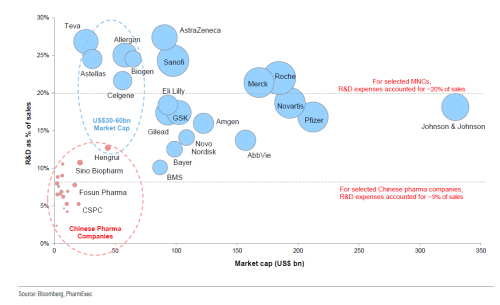

Interestingly, the MSCI China Healthcare Index had a cumulative market value of $275 billion at the end of 1Q19 as compared to the U.S. Healthcare Select Sector Index of $3.5 trillion. The publicly traded Chinese biotech companies have historically invested considerably less in R&D as a percent of revenues (see below); given the stated goals to challenge U.S. and European pharmaceutical companies in the novel therapeutic development, one should expect that relationship to change materially. One immediate implication of this is likely to be a more robust market opportunity for AI and Real World Evidence (RWE) solutions that will improve drug development processes.

One last observation unrelated to healthcare which involves the level of Chinese debt, a constant source of concern among investors which is now generating heighten levels of official anxiety. The National Development and Reform Commission recently observed that high yield debt issuances doubled in 2019 over 2018 to $51.8 billion, 90% of which was issued by real estate developers. Total debt issuances in 2019 are estimated to be over $67 billion. Outstanding real estate debt alone is now estimated to be $571 billion, $28 billion of which comes due in 2020 according to Dealogic. The Financial Times this weekend highlighted that of the 43,600 desks at WeWork China in Shanghai, 35.7% of them were unoccupied (worse in Shenzhen with 65.3% unoccupied). Slowing growth and elevated levels of debt are something to watch closely.

A fascinating article one of many you have written

Tremendous insight!

Very informative!

Thank you!