The 3Q17 year-to-date funding data point to several important emerging themes and may clarify where the broader healthcare technology sector is heading. Through nine months the investment pace has been nothing short of robust with StartUp Health and Rock Health data tallying $9.0 billion and $4.7 billion, respectively, although there are signs of recent moderation ($2.5 billion was invested in 3Q17 according to StartUp Health, suggesting a more muted 4Q17 level).

More specifically, according to StartUp Health there are now three sub-sectors of the healthcare technology sector which have already attracted more than $1.0 billion of capital YTD (Big Data/Analytics ($1.3 billion), Personalized Health ($1.2 billion), Medical Device ($1.0 billion)), underscoring both the maturity and depth of these market opportunities. Notably, seed investment activity was 28% of the total deal count 2017 YTD, which is the lowest annual level since 2010, further suggesting that we are now entering a period of consolidation, when emerging category leaders come of age, separating themselves from the pack. Furthermore, average deal size increased from $14 million in 2016 to $18 million YTD 2017. In 2016, Accenture determined that only ten companies accounted for 38% of all private equity fundings in the healthcare technology sector; expect to see that continue in 2017.

The strong fundamentals are not lost of public stock investors either. The Leerink Healthcare Tech/Services stock index increased 30% over the first three quarters of 2017, trading at a heady 15.5x and 15.3x 2017 and 2018 EBITDA, respectively. EBITDA margins for 2017 and 2018 for this cohort are estimated to be 23.4% and 20.2%, underscoring the profitability of the successful companies in this sector. Accordingly, aggregate revenue growth forecasts for that same group of companies in 2017 and 2018 are 19.1% and 15.3%, which implies 4.3x and 3.7x 2017 and 2018 valuation multiples of revenue.

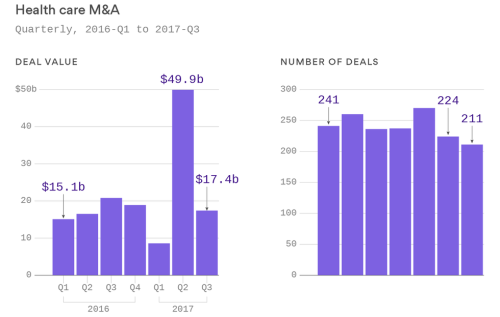

One emerging paradox then is the relative lack of M&A activity in the healthcare technology sector, particularly considering the growth characteristics of the sector and acquirers with strong public currencies. TripleTree tracked 242 closed M&A transactions in 3Q17, although only 45 disclosed deal metrics; notably, the average revenue multiple in those transactions was 2.8x, meaningfully below the level of publicly traded companies in the sector. Total 3Q17 transaction volume was $16.2 billion which was a decrease of 45% from the prior quarter. Crosstree Capital Partners identified only 7 deals in 3Q17 with announced values of greater than $250 million, suggesting that much of the M&A activity was small, likely distressed sales of companies that were not able to scale. This is not surprising given the amount of venture capital that was deployed in 2015-2016, which afforded start-ups only 18-24 months of runway.

Another topical item has been “healthcare Artificial Intelligence” (AI) and what the likely impact of these solutions will be on healthcare. Rock Health estimates that stand-alone AI vendors will account for nearly $500 million of investments in 2017 (or nearly 10% of all activity) and that 80% of those companies are principally B2C focused. Anecdotally, with increased customer fatigue and elusive ROI for many of these products, we may be at an inflection point here as well. AI vendors will need to modify business models to allow them to take on more risk, aligning with customers to help solve fundamental clinical issues versus simply flagging at-risk members / patients. According to a Pricewaterhouse Coopers (PwC) industry framework, healthcare AI is mid-way through the second of four phases (“Data Fusion” phase) when customers are experimenting with AI solutions and industry alliances emerge. By 2020, PwC calls for the “Commercialization” phase when meaningful clinical impact will start to be realized. Soon will come the day when AI is no longer tracked separately and it is simply part of every healthcare technology company’s product offering.

Two other important themes presented themselves over the last few months: (i) dramatic and large company M&A activity (CVS – Aetna, Humana – Kindred, UnitedHealth – DaVita, etc); and (ii) quite an accommodative regulatory environment. At its essence, the transition to value-based models is driving providers and payors to manage greater elements of the patient / members’ healthcare journey. With possible Medicare and Medicaid cuts coming, the specter of very significant pricing pressure is very real. And recently introduced is the competitive concerns of what a healthcare-focused Amazon means to established businesses as the patient / member becomes even more of a healthcare consumer. If nothing else, with scale should come a stronger hand when negotiating customer contracts.

Undeniably the new FDA Commissioner Gottlieb has created a more accommodative regulatory framework for healthcare technology start-ups, from establishing pre-certification pilot programs to lowering the hurdles for direct-to-consumer genetic health risk tests. Expect to see a wave of novel diagnostic devices, disease management platforms, monitors, etc be introduced to the market without the historic burdensome regulatory pathway. Notably, in 2017 the FDA cleared 51 connected health devices. Additionally, the Creating High-Quality Results and Outcomes Necessary to Improve Chronic Care Act (CHRONIC Act) was passed in 3Q17, which expanded Medicare coverage for telehealth services.

Arguably, the two themes above are beneficial to healthcare technology start-ups. For the established companies, new revenue opportunities and new risks that need to be managed require innovative new products and solutions, sourced (or acquired) by start-ups. Coupled with a more forgiving regulatory environment, expect to see faster “time to market” which has been one of the chronic issues confronting many early-stage healthcare technology companies – rarely is it that the product does not work but rather a window was missed due to poor product / market alignment.

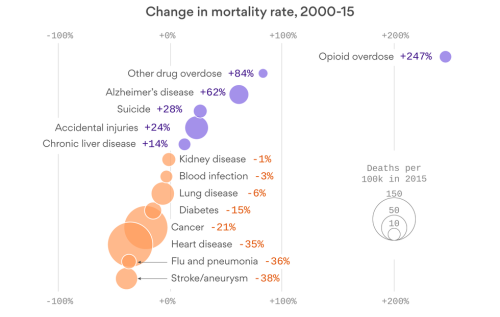

Another interesting perspective to handicap where investor focus will be over the next few years is to look at the gravest threats to the human condition today. Quite clearly, we are struggling with a national addiction crisis as well as confronting a host of devastating neurodegenerative diseases. It is also more understandable why behavioral issues are so front and center in healthcare VCs minds now. As shown below, our biotech VC brethren have had a dramatic impact on many other chronic diseases.

So, as we turn the page on another year, there are several emerging opportunities that should continue to gain traction. At their essence is the imperative to have greater presence, real-time, “in line” healthcare infrastructure, implying a handful of elements:

- Dramatically greater level of data sharing with improved interoperability, particularly in the clinical setting, needs to improve after nearly a decade since widespread electronic medical record adoption, to address widespread data asymmetry in healthcare

- Novel care delivery models will continue to develop and be more robust, from telehealth to other modalities to meet the patient where it best suits him / her, particularly in the home – healthcare system needs to move from a paradigm of healthcare consumption to one of healthcare experiences, and price accordingly

- Deeper levels of patient engagement, both active and passive, acknowledging that healthcare complexity requires that much of the coordination and navigation will need to be done on behalf of the member / patient / consumer

- Employers will continue to play a larger role in what defines success for healthcare technology companies, as the employer has clear and measurable ROI requirements

- Computational care driven by AI and personalized medicines

Thanks, Michael. As always, an insightful look at the markets. Look forward to continuing to work together to solve health problems. All the best for a spectacular 2018!

Great read and insights Michael. Love the part about “Deeper levels of Patient Engagement”