More than 18% of Americans at the end of 2020 were responsible for $140 billion of overdue medical debt, which is debt that has already been sent to collection agencies and, in many of those cases, is a crippling overhang to those individuals. Medical debt is the single largest source of debt that these agencies handle. “High medical debt” is defined as debt that is more than 20% of annual household income, and while only 4% of U.S. households fall into this category, the U.S. Census Bureau estimates that 11.3% of households in poverty have “high medical debt.” Coupled with last month’s Journal of the American Medical Association report finding that wealth correlates directly to longevity, the minatory impact of medical debt on the overall state of U.S. healthcare must be better understood.

While doctor visits and diagnostic procedures are relatively inexpensive, their prevalence contributing to the medical debt issue is very high per a 2016 Kaiser Family Foundation study. This likely has the unfortunate downstream implication of people deferring necessary primary care and preventive procedures, leading to more expensive future health conditions. Not surprisingly, issues concerning hospitalizations were identified as the most significant expense items, and likely were least avoidable, further contributing to an aversion to engage with the healthcare system.

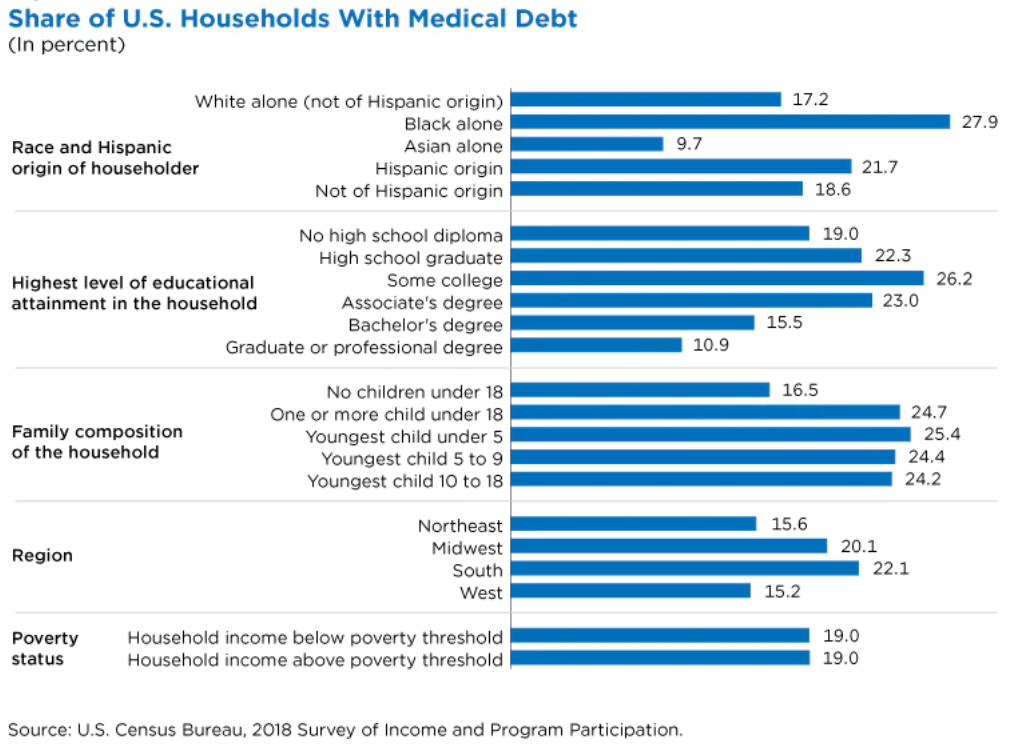

Perhaps not surprising, the demographics of those confronting medical debt burdens tend to skew towards groups who have uncertain paths to wealth accumulation or historically have been disenfranchised. Another shared attribute: those with high levels of medical debt tend to reside in states that have chosen to not expand Medicaid programs. Per capita medical debt in 2020 in those states is $375 greater than the other states and is 30% higher than before the adoption of the Affordable Care Act. Per capita medical debt in zip codes with the lowest household incomes was $677 as compared to $126 in the highest income zip codes. In 2018 the U.S. Census Bureau reported that nearly 38% of households with net worth below $0 had medical debt while less than 7% of households with a net worth greater than $500k had medical debt. Last month the Stanford Institute for Economic Policy Research published an analysis of medical debt by county (below).

This debt load tends to be more prevalent and greater in size for those least financially equipped to handle it. The Kaiser study found that 53% of the uninsured reported issues with medical debt versus only 20% of those with health insurance. Only 17% of those with medical debt obligations even had savings or investment accounts. Families with lower educational levels and families with young children tend to be burdened more often with medical debt. According to a 2014 analysis by the Consumer Financial Protection Bureau, 19.5% of all credit reports flag at least one outstanding medical debt obligation while 22% of all consumers have medical debt in collection.

The disparities have been exacerbated by Covid; over the past 25 years, the personal savings rate nationally has hovered between 5% – 7% but spiked with the pandemic lock-downs. While it is now trending back towards 10%, much of this recent wealth accumulation has benefited the higher income brackets, helping them to further service any existing debt loads.

To be clear, the U.S. consumer is perpetually navigating a minefield of debt obligations. At the end of 2Q21, overall household debt stood at $14.96 trillion, with mortgage debt accounting for the largest component at $10.44 trillion. Nearly 45% of the outstanding mortgage balance was originated in 2020 with the dramatic refinancing boom, allowing qualified borrowers to further “create wealth” through lower debt servicing demands (to say nothing of the extraordinary appreciation of real estate assets over the last two years). The outstanding cumulative credit card balances at the end of 2Q21 was $787 billion, which is quite a bit lower than the $927 billion in 4Q19 (before the pandemic), further highlighting the dramatic liquidity enjoyed by more affluent consumers.

An insidious characteristic of medical debt is relatively high default rates which sit unresolved on consumers’ credit reports. Paying a healthcare provider for services rendered months or years earlier will rank lower than keeping a house or buying food. The lack of price and cost transparency to the consumer contribute to the perception of the capricious nature and randomness of healthcare bills. The U.S. healthcare system is the most expensive of the 36 nations in the Organization for Economic Co-operation and Development which is not lost on most U.S. healthcare consumers, some of whom may simply feel over-charged. According to a recent Axios analysis, the healthcare industry enjoyed a 9% profit margin in 2Q21.

The “rich versus poor” debate is playing out among countries too. In developed countries the fully vaccinated rate is ~40% while it is just 11% in the developing economies, per a recent New York Times analysis. A great fear of this disparity is that new variants will continue to cycle around the globe. If this were to be the case, the International Monetary Fund estimates the global cost over the next four years to be $4.5 trillion in lost gross domestic production. The cost of poor healthcare and structural debt to a country can be devastating. Case in point is Haiti, which has suffered enormously over the last decade. Over 200 years ago, France demanded a 150 million franc payment for its independence, a crushing burden that the country is still trying to service.

Ironically, all of this is playing out against a backdrop of exceptional financial liquidity. Globally, corporations have $6.84 trillion of cash on-hand at the end of 2Q21 according to S&P Global data, which is 45% greater than the annual average over the five-year period pre-Covid. Over $16.5 trillion of debt globally now trades at a negative yield, according to Barclays. Simply unprecedented. All of this liquidity has led to a global M&A boom with $855 billion of deal activity in 2Q21 (Pitchbook), an increase of 12% over 2Q20.

With greater income and wealth inequality analysts anticipate greater disparities in health outcomes. While perhaps controversial, policies that lessen the medical debt burdens, thereby lessening the disparities, arguably should improve overall public health. While $140 billion of medical debt is an extraordinary number, in the context of a nearly $4 trillion U.S. healthcare system and nearly $15 trillion of household debt, one might dream that policy makers could architect a solution. In the face of the pandemic, over 11.8 million loans were approved as part of the Paycheck Protection Program (PPP) which had a total of $953 billion available for forgivable loans. It can be done.