Good God, everywhere you look there is bad news. Obviously, other than for the public equity markets, the question now is not can it get any worse (yes, which will likely be revealed in the May data) but rather, when might we start to see a recovery. The venture capital investment activity over the course of prior corrections may be an interesting indicator for what to expect over the balance of 2020.

But first, what did we see this past quarter? Overall, $34.2 billion was invested in 2,298 companies which was consistent with 1Q19 activity and suggests that at least at the outset of the year, the investment pace was likely to be in line with 2018 and 2019 levels. Upon closer inspection, one can see a marked decline in the number of deals, implying a significant increase in the average round size ($11.4 million in 2019, $14.9 million in 1Q20).

Valuations in 1Q20 were reasonably resilient as early stage and late stage investments were mostly flat in the quarter when compared to all of 2019: $28.0 million vs $29.4 million in early stage and $75.0 million vs. $80.0 million, respectively. The seed and angel stage pre-money valuations hovered between $7.5 – $8.0 million. According to Fenwick & West, the increase in share price over the prior round were 117%, 76% and 46% in January, February, and March, respectively, clearly underscoring more compression on valuations as 1Q20 progressed. In March 2019, the step-up was 63%. Flat may soon be the new “up round.”

There does appear to be a greater prevalence of downside protection terms such as full-ratchet antidilution, liquidation preferences, pay-to-play, and deeper discounts on bridge loans – all of which serve to provide greater investor protection. This also reflects a more challenging fundraising environment coupled with expectations for more modest exit valuations. Corporate venture capital (CVC) groups tend to retreat quickly when market conditions deteriorate, which appears to be the case now. According to Global Corporate Venturing, CVC participation decreased by 21% and 12% in terms of number of investments and amount invested in March when compared to a year earlier.

The closely watched Silicon Valley Venture Capitalist Confidence Index has never been so low, registering a 2.33 (on a 5-point scale) down from 3.60 at the end of 2019. This 35% decline is the greatest decrease in the 16-year history of the survey and eclipsed the prior low point of 2.77 set in 4Q08, amid the Great Recession.

One other contributing factor to the chaos before us. Typical fundraising rounds provide companies with 12 – 18 months of cash “runway.” The significant investment activity of 2018 and 2019 (according to Pitchbook there were nearly 22,900 financings over those two years) has created an extraordinary number of companies poised to come back to market. Pitchbook estimates that there are approximately 7,200 that now need to raise additional capital.

Silicon Valley Bank (SVB) estimates that 82% of all venture-backed companies were founded by entrepreneurs who have not experienced a recession – a dynamic exacerbated by the fact that 61% of venture firms today have not had to navigate such a downturn. For venture firms that have median fund size greater than $100 million, SVB determined that 52% of them have not had to manage through a recession. Since March 11, when the coronavirus was declared a pandemic by the World Health Organization, 45,243 people were laid off by start-ups according to the “Layoffs.fyi Coronavirus Tracker.” And all of those participants are now staring at the chart below (and that is not the more inclusive U6 Unemployment Rate which is 22.8%)…

Twenty years ago, there was another venture industry correction. In 2000, the quarterly investment pace was between $25 – $27 billion. In 2001, with the correction well-underway, the quarterly investment pace dropped to nearly $10 billion, only to drop to a $4.0 – $5.0 billion quarterly pace starting in 2002 and lasting for the next four years. Analysts peg that market peak to have been in 2Q00, suggesting that investors in 2001 were mostly only funding those existing portfolio companies deemed able to weather the storm. Once the immediacy of the crisis abated, a more normalized level of investment activity was only around 20% of the high-water mark set in 2000.

During the Great Recession a dozen years ago, there was a more modest re-set in overall investment activity, in part due to the fact that the venture industry never fully recovered from the Dot.com debacle. Total investment in 2007 and 2008 was $36 billion annually, decreasing to $27 billion and $31 billion in 2009 and 2010, respectively.

Arguably, 2020 looks more akin to 2001 than 2009, given that the industry is coming off of a very robust pace in 2018 and 2019 a la 1999 and 2000. The step-down is likely to be steeper, obviously made enormously more complicated by the fact that investors are not able to actually meet with entrepreneurs and visit the prospective companies.

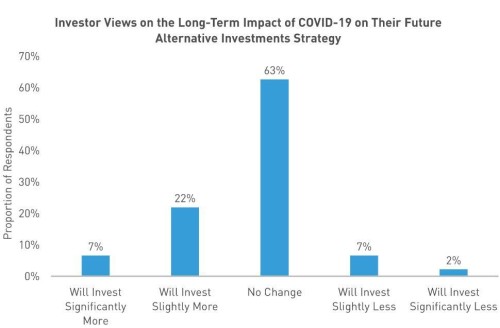

One mitigating consideration will be the appetite of limited partners to commit to new funds. In 1Q20, the fundraising environment was reasonably strong as 62 venture funds raised $21.0 billion. Of that total, 70% was committed to funds greater than $500 million in size, suggesting further consolidation around larger established venture franchises. There were only nine new investment firms, raising $1.1 billion, further underscoring the consolidation. In fact, limited partner sentiment has shown to be quite resilient, at least at the outset of the pandemic and for branded firms. According to a recent Preqin survey (below) of 110 institutional investors, only 9% will reduce commitments to alternative asset classes. Notwithstanding that, over $4.65 trillion is now held in money market accounts, which is $700 billion more than the greatest level during the Great Recession, punctuating the overall flight to safety.

The investment activity in China may also provide guidance as to what the entrepreneurs in the U.S. should expect over the next few quarters. Arguably, the impact of the coronavirus hit the Chinese market at least 90 days before the U.S. According to Fortune, venture investment in the technology sector declined 30% in 1Q20 from the prior year ($16.8 billion vs. $24.0 billion) and the number of transactions declined 45% to 634 deals in 1Q20. A fairly rapid and dramatic correction.

None of this is to suggest that the correction and subsequent recovery will be swift or predictable. Given the level of systemic debt (several trillion dollars) that has been issued and the global sweeping nature of the pandemic, the path forward will be very difficult. The capital markets are seeing a level of financial distress not seen before.

With the Congressional Budget Office now forecasting a U.S. budget deficit that will be $3.7 trillion this year and public debt to now be 101% of GDP, the consumer has been upended as economic activity continues to drop precipitously. The International Monetary Fund in its recent World Economic Outlook has already called this the most devastating economic crisis in nearly a century, and it is just starting. The ultimate impact is near-impossible to even forecast. Already it is believed $9 trillion of economic value has been lost globally even should there be a rapid recovery in 2H20; that is the equivalent of the GDP of Japan and Germany combined.