By nearly every measure, 2018 was a banner year for the venture capital industry, particularly in the healthcare technology sector. Over $130 billion of venture capital was invested across all sectors, easily eclipsing the prior high-water mark in 2000 and nearly 4.8x of what was invested a decade ago. While certain sectors may now be demonstrating bubble-like tendencies, the data also reflect the activity of Softbank’s ~$100 billion Vision Fund and other late start cross-over investors. In the healthcare technology sector, according to Rock Health, $8.1 billion was invested in 368 companies which is notably greater than the $5.7 billion invested in 2017 (StartUp Health pegs 2018 at $14.8 billion globally).

But have we entered a healthcare technology bubble?

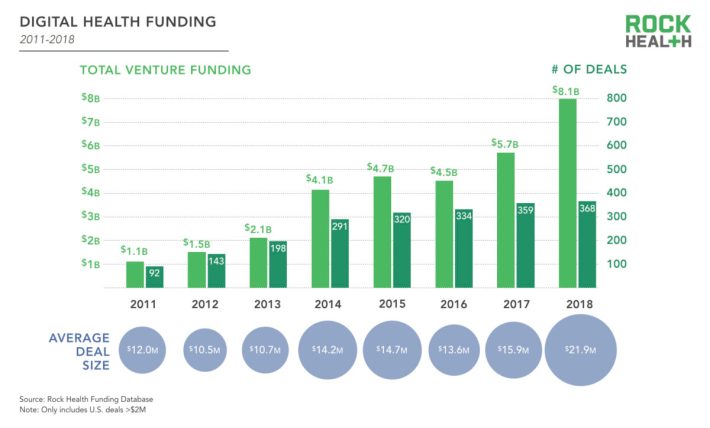

First, some context. Over the past five years, healthcare technology investors have funded consistently between 300 – 375 companies each year. Between 2014 – 2016, the amount of capital invested annually ranged between $4.1 – $4.7 billion. The average deal size spiked to $21.9 million in 2018 but otherwise had been consistently between $14 – $16 million since 2014. In 2011, 92 healthcare technology companies raised $1.1 billion (average deal size was $12.0 million). Of the 368 financings in 2018, only 11 were greater than $100 million in size. Importantly, there were only 110 M&A exits and no IPOs in 2018.

Notwithstanding the herd mentality tendencies of venture capitalists and that chronically there is a “capital absorption” issue (that is, too much capital invested too quickly in any sector depresses returns), the healthcare technology sector does not exhibit the classic characteristics of a bubble. In 2011, this sector accounted for just over 2.4% of all venture dollars invested, reaching only 6.2% in 2018. Classic bubble markets tend to be awash in hype – either at the novelty of the companies, the seductive rates of growth, dramatic and sudden liquidity, or the ability for a “quick flip” (see all things crypto currencies) – arguably none of these attributes are present today. Importantly, nearly 60% of all healthcare technology investors in 2018 had invested in multiple companies in the sector, suggesting some level of investor understanding and commitment to the sector.

Clearly, healthcare is an enormous market going through a remarkable transformation and that has drawn a lot of attention. At over $3 trillion of annual spend, much of which is being reapportioned between new and incumbent players, healthcare is nearly 15x the size of the U.S. advertising industry, estimated to be approximately $200 billion. And look at the staggeringly valuable companies created over the last two decades as the advertising industry was rearchitected (see Google, Facebook, etc). Furthermore, with the Democrats’ successes in the mid-term elections, many analysts anticipate expanded public healthcare proposals which will further drive interest and activity (see New York City’s recent $100 million proposal for expanded primary care services).

Many start-ups in the healthcare technology sector today are relying on quite well-understood technologies which have been widely utilized across other sectors for many years; often times the innovation is around the novelty of the business model, meaningfully limiting the true technical product development risk. The problems healthcare technology entrepreneurs are solving are quite obvious and indisputable (need to lower costs, improve outcomes). Overall healthcare industry growth rates are modest and somewhat predictable. The battle is to reallocate dollars to more efficient, more efficacious solutions and approaches.

And while there are some encouraging signs about investor liquidity and exits, there certainly has not been the explosion of irrational outcomes far in excess of underlying fundamentals. Venture capitalists across all sectors always bemoan the lack of consistent exits; recent exit activity in the healthcare technology sector suggest prudent consolidation of sub-scale companies (most of the exit values were not disclosed, strongly suggesting underwhelming outcomes). However, this does not suggest that many of the later stage private financings today are not fully valued and priced for perfection.

Arguably, the healthcare technology sector is showing signs of maturation. Larger round sizes may simply reflect that many companies are now scaling. Undoubtedly, it also reflects that some healthcare technology companies have lower gross margins due to a greater level of (lower margin) services and longer sales cycles, all requiring more capital. The sales of Flatiron to Roche for $2.1 billion and PillPack to Amazon for ~$750 million underscore the attractiveness of healthcare technology companies to companies in adjacent sectors, suggesting a depth to the acquirer universe for break-out companies in this sector.

Public stocks in this sector have also performed quite well: the Rock Health “Digital Health” Index increased 21.6% in 2018 which compares very favorably to the S&P 500 which declined over 6% for the year. Strong public stock performance should create a cohort of acquirers with attractive currency for further consolidation. Notwithstanding 4Q18 market volatility, the healthcare industry ended 2018 trading at 20.0x P/E versus 17.7x for the S&P 500. And so far, so good in 2019.

It may be instructive to look at the funding data for the “cleantech” sector in the 2000’s. Like healthcare, the energy sector is a large regulated industry which also attracted a lot of venture capital investor interest. Unlike healthcare, though, these investors took on significant technical risk with less clear business models, and yet it still took nearly a decade to hit the peak number of companies funded annually (just over 700 or more than 7x the number funded ten years earlier). While that number declined to below 500 over the ensuing five years, the amount of capital invested stayed relatively constant at around $5.0 billion annually. The high-water mark was in 2011 when nearly $7.5 billion was invested; notably that would have been well over 16% of all venture investment activity, which was clearly not sustainable.

Determining whether this is a bubble is more than an academic debate. Other bubbles have ended fabulously badly, bursting and leaving oily residue everywhere, so it is instructive to search for other bubbles to see if there are relevant parallels (and one may not need to look too far…)

- Aforementioned crypto currency: Bitcoin now trades at $3,530 per token, down from all-time high of $19,783 on December 17, 2017. How many of you had heard of Bitcoin in January 2013 when a token traded for $13.30? Ever used one?

- It is estimated that venture capitalists have funded over 1,000 artificial intelligence (“AI”) start-ups in 2018, up from 291 five years ago. Participants at the World Economic Forum in Davos, Switzerland last week had 11 AI panels from which to choose.

- According to the Institute of International Finance, global debt reached $244 trillion at the end of 2018 (nearly 80x the U.S. healthcare industry) which was estimated to be 318% of global GDP – a very frightening debt load.

- The Chinese bond market is $12.7 trillion of which $4.0 trillion is corporate debt. While there was only $23.3 billion of corporate bond defaults (0.6% of total outstanding) in 2018, this was more than the prior four years combined – and likely is significantly understated.

- U.S. corporations have taken on nearly $9.0 trillion of debt since the Great Recession. Just since 2017, the number of companies rated one level above junk bond status increased 247% but Fitch Ratings has only downgraded 7% of them. Hmmm.

- This month the 5-year Treasury yields were less than the 2.25% – 2.5% that the Fed targets for rates banks pay for overnight loans. This inverted yield curve has been an unshakable predictor of recession. Gulp.

The healthcare technology sector took no one by surprise, is addressing profoundly important and obvious problems, and should be able to productively deploy significant capital – if deployed thoughtfully.

Check out a recent Rock Health podcast for additional debate about whether the healthcare technology sector is in a bubble…

They do need to come a long way in reducing cost and with the billions they take in every year they have the resources to. Hopefully foreign competition will do more to effect this.

Pingback: 7 Innovative Technologies Making Healthcare More Productive and Efficient - Electronic Health Reporter